Why a 50-Year Mortgage Isn’t Actually Affordable

Nov 9, 2025

Quick take

There’s been buzz this week around a proposed 50-year mortgage that’s being pitched as a fix for housing affordability. It’s not law, and it may never be. But for first-time buyers, it’s still worth paying attention to, because it highlights how “affordability” can be misleading.

What’s the deal with a 50-year mortgage?

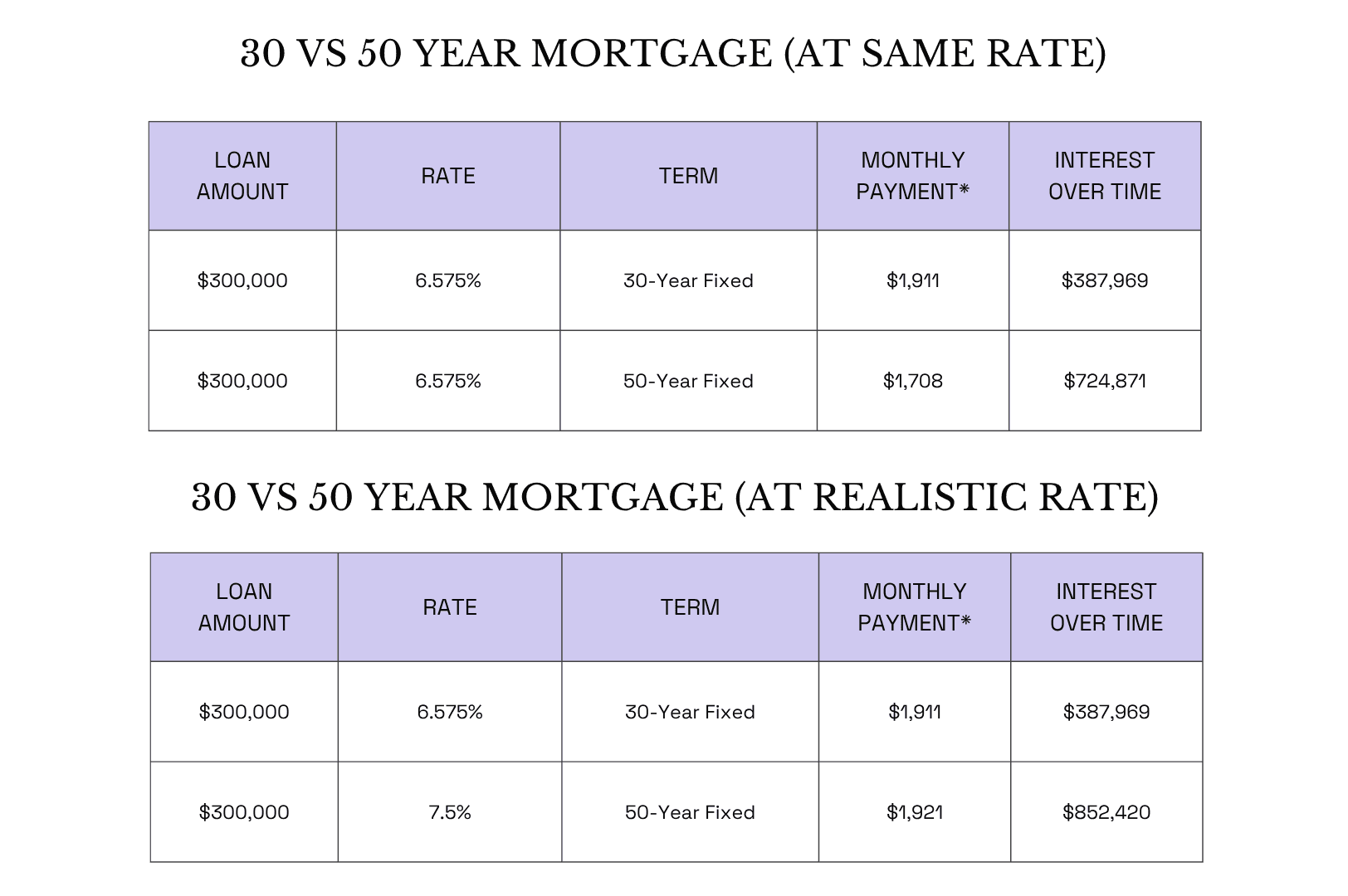

The proposal suggests extending fixed-rate mortgages from the usual 30 years to 50 years to lower monthly payments. Let’s put some real numbers behind it.

Here’s what the difference looks like for a $300,000 loan at today’s average 30-year rate of 6.575% — first assuming both loans share that rate, and then with a more realistic bump to 7.5% for the 50-year term.

*Principal + interest only.

Even if rates stayed the same, stretching to 50 years means paying hundreds of thousands more in interest, just to shave a couple of hundred off the monthly payment. And once you factor in a higher rate (which is almost guaranteed), that “affordability” disappears entirely.

Bottom line: a longer loan doesn’t make the home cheaper — it just makes your debt last longer.

Why a longer mortgage doesn’t equal more affordability

1. You build equity painfully slow

Most early payments go straight to interest — not principal. Stretching your loan to 50 years means it’ll take decades longer before you actually own a meaningful portion of your home.

2. You’ll pay significantly more interest overall

Even with the same rate, you could end up paying hundreds of thousands more across the life of the loan. Lower monthly doesn’t always mean a better deal.

3. It’s not even approved (yet)

This would require major regulatory changes. Right now, 30-year mortgages are the max length under typical “qualified mortgage” rules. So even if this proposal gets attention, it’s not available to you today, and might never be.

4. It could inflate home prices long-term

When people can borrow more, sellers often charge more. So while the 50-year term could make homes “seem” more accessible, it may actually keep prices high and affordability low for everyone.

5. You lose flexibility

If you want to move, refinance, or use your equity in the next decade, a 50-year loan keeps you tethered much longer. That can limit your options down the line.

Real-talk takeaway

A 50-year mortgage might sound like a creative fix, but it’s really a delay tactic that kicks affordability down the road while increasing long-term debt.

At Entitled, our goal is to help you see the full picture, including the fine print, the trade-offs, and the real numbers behind every big housing headline.

If you’re trying to figure out what’s actually affordable for you, start with tools like our Homebuying Journey Checklist and use our built-in mortgage calculator to compare loan lengths side-by-side. Try them now →

Heads up: This isn’t legal or financial advice—just helpful info to make things make more sense.